Banks’ climate scenarios are “wildly missing or underestimating potential risk”

Editor’s note: U.K. researcher Tim Lenton was a busy man at last week’s Climate Week in New York. His message was stark: Banks, including central banks, insurers and sovereign wealth funds must dramatically revisit how they assess climate risk.

Current climate change scenarios used by central banks are “wildly missing or underestimating potential risk,” says Lenton in an interview with Green Central Banking. The University of Exeter professor is one of the authors of a recent report which finds that present financial models fail to capture the reality of climate risks.

The report, The Emperor’s New Climate Scenarios – A Warming for Financial Services, warns that the financial services sector must act urgently to effectively consider and embed the impact of climate change into risk management.

One of the major obstacles to understanding and preparing for climate financial risk globally is the lack of accurate and shared data, he says. Risk scenarios are only as good as the data and the existing models are missing key data, including who owns fossil fuel debts.

Lenton says there is a fatal flaw in traditional risk assessments developed from mainstream macroeconomics because these models miss essential data on climate risk.

“There’s a clear way forward to raise the bar of this kind of risk assessment research, but it needs some sociology and it needs some sort of support or willingness for participants to come together to tackle [accurate climate risk models],” he says.

Little scientific data in financial risk models

Lenton says there is a fatal flaw in traditional risk assessments developed from mainstream macroeconomics because these models miss essential data on climate risk.

Remarkably, present central banks and other financial institutions do not consider both financial and scientific data. What should be happening, he says, is climate scientists, migration specialists and financial experts together look at current financial models to see how they can be improved.

“Shared socio-economic pathways span a much wider range of the possible space of how things could develop,” he said.

Looking beyond 1.5 degrees to measure real climate risk

Other areas where central banks can improve climate risk models include looking at different variants of rising temperatures rather than the standard 1.5ºC that is often used to calculate climate risk. The reality is likely to be closer to 2.5 or 3ºC, he said. They could also use different versions of population demographics and various storyline changes for the future.

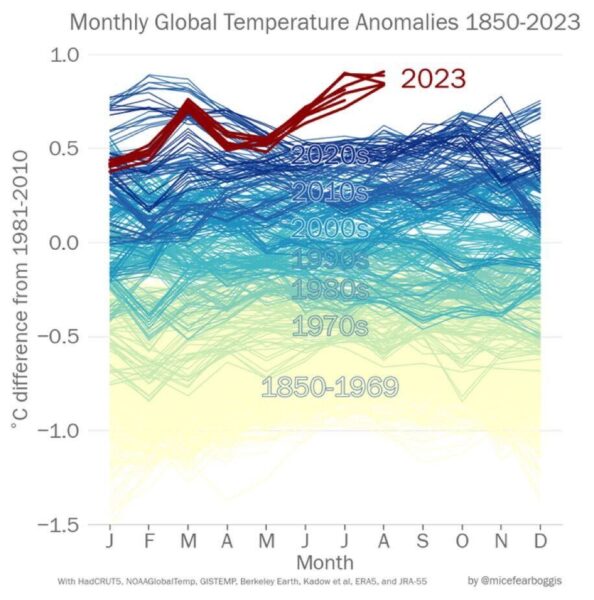

The world is passing through climate tipping points that could trigger abrupt and irreversible changes to the climate. For example, a recent report from two Danish researchers found that ocean currents that regulate the climate could collapse sooner than expected, leading to even more extreme weather events across the globe. That is the kind of data that needs to be part of climate risk modelling.

Lenton said it’s “blindingly obvious” that these extreme climate impacts are “increasing non-linear,” adding “I hope they’re not, but we could be on the cusp of suddenly much more clear impacts on health, well-being and the labor force in some key cultures and geographies,” he said.

These new threats must now be incorporated into financial risk modelling that the world’s largest and most influential banks use to protect trillions in capital.

This article originally appeared in Green Central Banking.